Global Tampon Market Size, Share, Growth Analysis By Product (Radially Wound Pledget, Rectangular or Square Pad), By Material (Cotton, Rayon, Blended, Others), By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Pharmacy Stores, Online Retail, Hospital Pharmacies, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2034

- Published date: March 2025

- Report ID: 143792

- Number of Pages: 232

- Format:

-

Quick Navigation

Report Overview

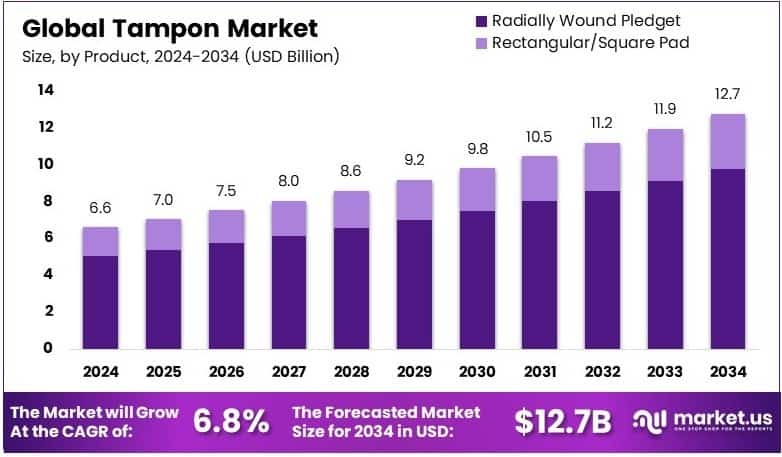

The Global Tampon Market size is expected to be worth around USD 12.7 Billion by 2034, from USD 6.6 Billion in 2024, growing at a CAGR of 6.8% during the forecast period from 2025 to 2034.

A tampon is a feminine hygiene product designed to absorb menstrual blood internally. Made from compressed layers of soft material, usually cotton or rayon, tampons are inserted into the vagina during menstruation. They offer discretion and comfort, allowing users to remain active with minimal inconvenience.

The tampon market encompasses the production and sale of tampons as a segment of feminine hygiene products. It addresses diverse consumer preferences regarding comfort, absorbency, and material, with a focus on safety and accessibility. Market dynamics include regulatory impacts, demographic trends, and cultural shifts affecting product usage.

The tampon market is currently experiencing significant growth, primarily driven by heightened global awareness of feminine hygiene and an increasing focus on women’s health issues. Legislative efforts in the United States have notably advanced this cause; as of 2023, 26 states have enacted menstrual equity bills aimed at combating period poverty.

These legislative measures are critical as they not only provide menstrual products to incarcerated individuals and students but also work towards reducing or eliminating the sales tax on feminine hygiene products, making them more accessible and affordable.

This trend is not isolated to the United States; worldwide, the demand for tampons is rising due to several influencing factors. Notably, a report from the World Health Organization and UNICEF reveals a substantial challenge: approximately 780 million people lack access to improved water sources, and about 2.5 billion are without improved sanitation.

These conditions pose significant barriers to managing menstrual hygiene effectively, particularly in less developed regions, thereby increasing the reliance on and necessity for hygienic menstrual products like tampons.

The market dynamics are also shaped by the level of market saturation and competitiveness, especially in developed economies where numerous brands vie for a share of consumer attention. Despite the competition, opportunities abound as manufacturers innovate with eco-friendly materials and improved product designs that offer better comfort and protection, aligning with the increasing consumer preference for sustainable and health-conscious products.

Government initiatives play a pivotal role in shaping market prospects. Regulations and investments aimed at promoting menstrual health and ensuring the availability of feminine hygiene products can greatly influence market dynamics. These actions not only support public health but also encourage market entry and expansion by creating a conducive environment for businesses to innovate and grow.

Key Takeaways

- Tampon Market was valued at USD 6.6 Billion in 2024 and is expected to reach USD 12.7 Billion by 2034, with a CAGR of 6.8%.

- In 2024, Radially Wound Pledget led the product segment with 76.4%, owing to its superior absorption and widespread consumer preference.

- In 2024, Cotton dominated the material segment with 35.8%, driven by increasing demand for organic and hypoallergenic menstrual products.

- In 2024, Supermarkets & Hypermarkets held 28.7% of the distribution channel, benefiting from high consumer footfall and product accessibility.

- In 2024, Online Retail experienced significant growth, supported by the rising trend of e-commerce in personal care products.

- In 2024, North America dominated the market with 33.2% and a value of USD 2.19 Billion, fueled by strong brand presence and high product awareness.

Product Analysis

Radially Wound Pledget dominates with 76.4% due to its superior absorption and comfort.

In the tampon market, the Product segment is crucial and includes Radially Wound Pledget and Rectangular/Square Pad types. Radially Wound Pledget, the dominant sub-segment, holds a significant 76.4% market share in 2024.

This dominance is attributed to its design, which provides better absorption and comfort, making it highly preferred by consumers for its efficiency in menstrual management. This product type has been embraced for its ability to offer reliable protection, thereby gaining a substantial user base.

Rectangular/Square Pad tampons serve as an alternative to radially wound pledgets, catering to a niche market that prefers a different form factor. Although they hold a smaller market share, these products are pivotal in catering to diverse consumer preferences.

Material Analysis

Cotton dominates with 35.8% due to its natural and hypoallergenic properties.

The Material segment of the tampon market comprises Cotton, Rayon, Blended, and other materials. Cotton leads with a 35.8% market share in 2024, primarily due to its natural and hypoallergenic properties that appeal to health-conscious consumers. Cotton tampons are marketed for their comfort and safety, reducing the risk of irritation and allergies, which endears them to a broad demographic seeking natural menstrual solutions.

Rayon tampons are valued for their absorbency and smoothness, making them a popular choice among users looking for effective moisture management. However, concerns over safety and synthetic materials slightly limit their market share.

Blended materials combine the benefits of cotton and rayon, offering a balance of comfort and absorbency. These are significant for consumers looking for versatile menstrual products.

Distribution Channel Analysis

Supermarkets & Hypermarkets dominate with 28.7% due to their accessibility and variety of options.

The Distribution Channel segment includes Supermarkets & Hypermarkets, Specialty Stores, Pharmacy Stores, Online Retail, Hospital Pharmacies, and other channels. Supermarkets & Hypermarkets are the leading distribution channel with a 28.7% share in 2024, as they offer convenient access to a variety of tampon products under one roof, making it easier for consumers to compare and purchase based on their specific needs.

Specialty Stores provide specialized products and often offer expert guidance, attracting consumers who seek personalized shopping experiences. Although their market share is smaller, their impact on the tampon industry is reinforced by their specialized service.